When you think about how insurance companies control costs, you probably imagine higher premiums or tighter coverage rules. But one of the biggest ways insurers save money-and pass those savings along-is through bulk buying and tendering for generic drugs. It’s not flashy. It doesn’t make headlines. But it’s responsible for billions in annual savings and directly affects what you pay at the pharmacy counter.

Here’s the simple truth: generics make up over 90% of all prescriptions filled in the U.S. Yet they account for just 17% of total drug spending. That gap? That’s where the savings live. Insurers don’t just accept whatever price a pharmacy charges. They actively negotiate, bid, and lock in deals that can cut costs by 80% or more.

How Bulk Buying Works for Generic Drugs

Bulk buying means buying large quantities at once. But it’s not just about buying more-it’s about buying smarter. Insurers and pharmacy benefit managers (PBMs) group together thousands of prescriptions across millions of patients to create massive purchasing power. When a drug like metformin or lisinopril is prescribed hundreds of thousands of times a month, insurers don’t pay retail price. They go to manufacturers and say: "We’ll buy 10 million tablets this year if you give us a price below $0.10 per pill."

Manufacturers agree because volume guarantees steady sales. Even if they make less per pill, they sell far more. The math works. A drug that might cost $50 at a local pharmacy can be bought for under $5 in bulk. That’s not a discount-it’s a price collapse.

One study found that when a new generic enters the market, it saves an average of $5.2 billion in its first year. Just three first generics-lacosamide, pemetrexed, and bortezomib-each saved over $1 billion. That’s not luck. That’s strategy.

Tendering: The Competitive Bidding Process

Tendering is how insurers turn bulk buying into a competitive auction. Instead of signing a deal with one manufacturer, they open the floor. They say: "We need 5 million doses of atorvastatin. Submit your best price. We’ll pick the lowest that meets quality standards."

This isn’t theoretical. It’s standard practice. PBMs like OptumRx, Caremark, and Express Scripts run these bids every year. Contracts last 1-3 years. They include minimum volume commitments. And they’re binding. If the manufacturer doesn’t deliver, they pay penalties. If the insurer doesn’t meet the volume, they might lose the discount.

The result? For many generics, the price drops by 80-90% from the initial launch price. A drug that starts at $100 per pill can end up at $10-or less-after competition kicks in. The FDA tracks this closely. Their data shows that when multiple manufacturers enter the market, prices plummet fast. When only one or two make the drug, prices stay high. That’s why insurers push for multiple suppliers.

Why Some Insurers Still Overpay

Not all insurers save equally. Many still pay way too much because of how their PBM works. Most PBMs use something called "spread pricing." Here’s how it breaks down:

- The insurer pays the PBM $40 for a generic drug.

- The PBM pays the pharmacy $25.

- The PBM keeps $15 as profit.

That $15 spread? It’s hidden. The insurer doesn’t know the pharmacy was paid $25. They think they’re paying $40 for the drug. The PBM has no incentive to lower the price further. In fact, they’re often paid more if the drug is more expensive.

A 2022 JAMA Network Open study found that some generics on insurance formularies cost more than others with identical ingredients. Why? Because the PBM made more money off the higher-priced version. Insurers were unknowingly choosing the more expensive option.

This isn’t a glitch. It’s a design flaw. PBMs are owned by big insurers. So the money saved on drugs doesn’t always go back to the plan. It stays inside the corporate structure.

The Rise of Transparent Pricing

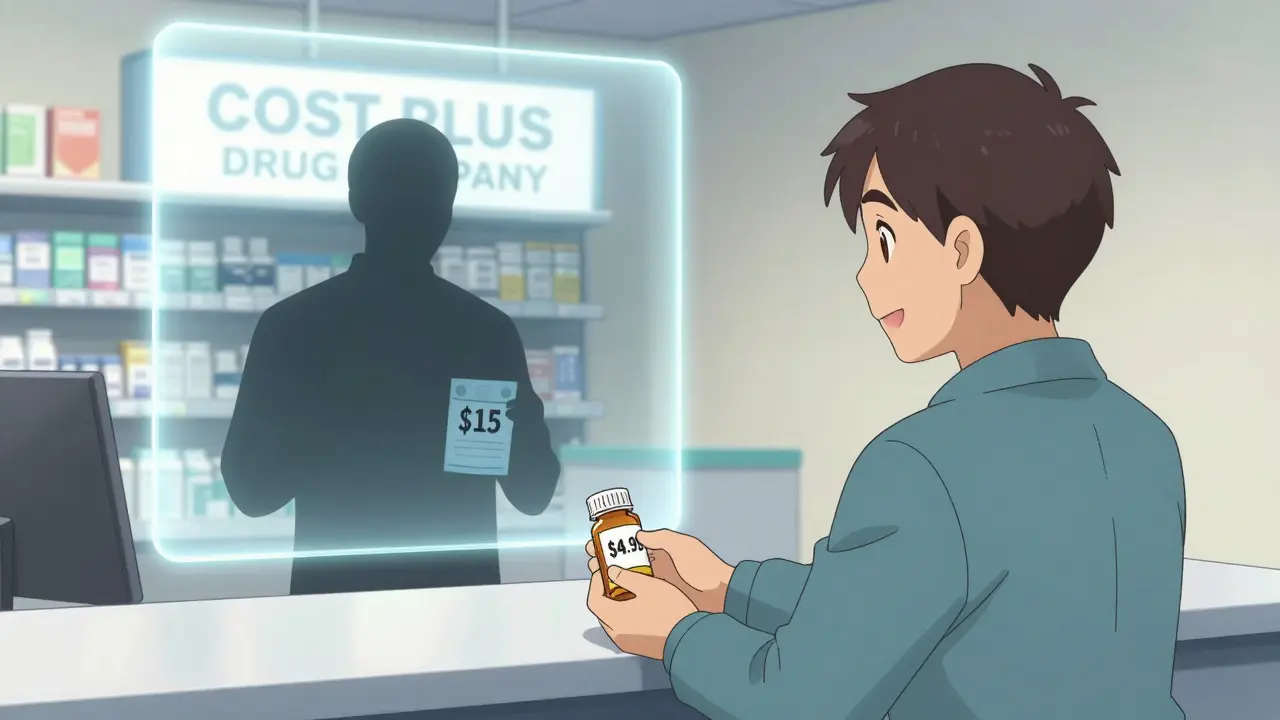

That’s why alternatives are growing fast. Companies like Cost Plus Drug Company and GoodRx cut out the middleman entirely. Cost Plus Drug Company sells generics at cost plus 15%. No spreads. No rebates. No secrets. A patient paying cash there might pay $4.99 for a drug that costs $87 under insurance.

And it’s not just individuals. Employers are starting to switch. Blueberry Pharmacy, for example, offers flat monthly pricing for generics-$15 for blood pressure meds, $10 for statins. No surprise bills. No formulary games. One user wrote: "My blood pressure medication costs exactly $15/month with no insurance surprises."

These models work because they’re transparent. You know what you’re paying. And when insurers see how much they’re overpaying through traditional PBMs, they start asking questions.

How Insurers Actually Find Savings

Smart insurers don’t just rely on bids. They analyze their own data. They look at which generics are costing the most. They compare prices across pharmacies. They check how many manufacturers make each drug.

Here’s a real example: A plan notices that their top-selling generic statin costs $32 per script. They dig deeper. They find another version-same active ingredient, same dosage, same manufacturer-that costs $8. The only difference? It’s not on their formulary. Why? Because the PBM gets a bigger kickback on the $32 version.

So they switch. They renegotiate. They move to the cheaper option. They save $24 per script. Multiply that by 50,000 scripts a year? That’s $1.2 million saved. All because someone looked at the numbers.

Studies show that quarterly reviews of generic spending can uncover hidden savings of 15-30%. That’s not magic. It’s basic auditing.

The Hidden Cost of Too Much Pressure

But there’s a dark side. When insurers push prices too low, manufacturers can’t make money. They stop producing. That’s what happened with albuterol inhalers in 2020. Prices dropped below $1 per inhaler. Manufacturers couldn’t cover production costs. Supplies vanished. Eighty-seven percent of hospitals reported shortages.

It’s a catch-22. You want low prices? Fine. But if you crush margins too hard, you kill supply. The solution isn’t to raise prices. It’s to diversify suppliers. Encourage competition. Avoid putting all your eggs in one basket.

What’s Changing in 2026?

The rules are shifting. In January 2024, the Centers for Medicare & Medicaid Services (CMS) required all Medicare Part D plans to disclose exactly how much they pay PBMs and how much PBMs pay pharmacies. No more hiding spreads.

California’s SB 17 law, passed in 2017, forced PBMs to reveal price differentials over 5%. Other states are following. Transparency is no longer optional-it’s the law.

Meanwhile, the FDA is speeding up generic approvals. More competition means more price drops. And companies like Navitus Health Solutions are reporting 22% lower generic costs for employers using their direct-buy model.

The future isn’t about bigger PBMs. It’s about smarter systems. Systems that reward savings, not spreads.

What This Means for You

If you’re on insurance, ask: "Is my generic drug the cheapest option?" Check GoodRx or Cost Plus Drug Company. Compare prices. You might find you’re paying 10x more than you need to.

If you’re an employer or plan sponsor, demand transparency. Ask your PBM: "What’s the spread? Who’s making money on my generics?" If they refuse to answer, it’s time to switch.

Generics were supposed to make medicine affordable. But without smart procurement, they’re just another place to overpay. The tools to fix this exist. The data is there. The savings are real. The question is: who’s going to use them?

How do insurers save money on generic drugs?

Insurers save money by using bulk buying and competitive tendering to negotiate lower prices with generic drug manufacturers. Instead of paying retail prices, they commit to large volumes of drugs in exchange for deep discounts-often reducing costs by 80% or more. They also switch to lower-cost alternatives with the same active ingredients and regularly audit their formularies to eliminate overpriced generics.

What is tendering in the context of generic drugs?

Tendering is a competitive bidding process where insurers or pharmacy benefit managers invite multiple generic manufacturers to submit prices for a specific drug. The contract goes to the lowest qualified bidder, often requiring a minimum purchase volume. This system drives prices down by encouraging competition and prevents any single manufacturer from charging inflated prices.

Why do some generic drugs cost more under insurance than cash?

Many insurance plans use pharmacy benefit managers (PBMs) that profit from "spread pricing"-the difference between what they charge the insurer and what they pay the pharmacy. If a PBM keeps a larger spread on a more expensive generic, they have no incentive to switch to a cheaper alternative. Cash prices at transparent pharmacies like Cost Plus Drug Company or GoodRx cut out the PBM entirely, revealing how much insurers are overpaying.

Can switching to a cheaper generic hurt my treatment?

No, if the drugs are bioequivalent. The FDA requires generic drugs to have the same active ingredient, strength, dosage form, and route of administration as the brand-name version. They must also prove they work the same way in the body. Switching to a lower-cost generic with the same active ingredient is not only safe-it’s standard medical practice.

What role do pharmacy benefit managers (PBMs) play in generic drug pricing?

PBMs act as middlemen between insurers, pharmacies, and drug manufacturers. They negotiate prices, manage formularies, and process claims. But many use opaque pricing models like spread pricing, which can incentivize them to favor higher-cost generics to increase profits. Transparent PBMs and direct-to-consumer models are now challenging this system by eliminating hidden markups.

Are there risks to pushing generic drug prices too low?

Yes. If prices are driven below production costs, manufacturers may stop making the drug, leading to shortages. This happened with albuterol inhalers in 2020, when extreme price pressure caused supply to collapse at 87% of U.S. hospitals. The solution is not to raise prices arbitrarily, but to ensure multiple manufacturers compete, keeping supply stable while maintaining low costs.

How can I find out if I’m overpaying for my generic medication?

Compare your insurance copay to the cash price on GoodRx, Cost Plus Drug Company, or Blink Health. If the cash price is lower, your insurance isn’t getting you the best deal. You can often pay cash at the pharmacy and save 50-90%. Also, ask your insurer or PBM to disclose the price they paid for your drug versus what you paid-transparency laws now require this in many states.

Graham Holborn

Hi, I'm Caspian Osterholm, a pharmaceutical expert with a passion for writing about medication and diseases. Through years of experience in the industry, I've developed a comprehensive understanding of various medications and their impact on health. I enjoy researching and sharing my knowledge with others, aiming to inform and educate people on the importance of pharmaceuticals in managing and treating different health conditions. My ultimate goal is to help people make informed decisions about their health and well-being.